WASHINGTON DC – For much of the 20th century, the American Dream followed a familiar path.

Graduate from school. Find a good job. Buy a home. Raise a family. Save for retirement. Leave your children better off than you were.

It wasn’t easy, and it wasn’t equally available to every American. Baby Boomers faced recessions, double-digit inflation, factory layoffs and economic uncertainty. Many Americans—including women and minorities—also encountered barriers that limited opportunities available to others.

Yet economists generally agree that for many middle-class families, the path to building wealth was more attainable than it is today.

As the United States marks the 250th anniversary of the Declaration of Independence, a growing body of economic evidence suggests Millennials face a much steeper climb.

The numbers tell a striking story.

The median first-time homebuyer is now 40 years old—the oldest since the National Association of Realtors began tracking the data. First-time buyers account for just 21 percent of all home purchases, another record low.

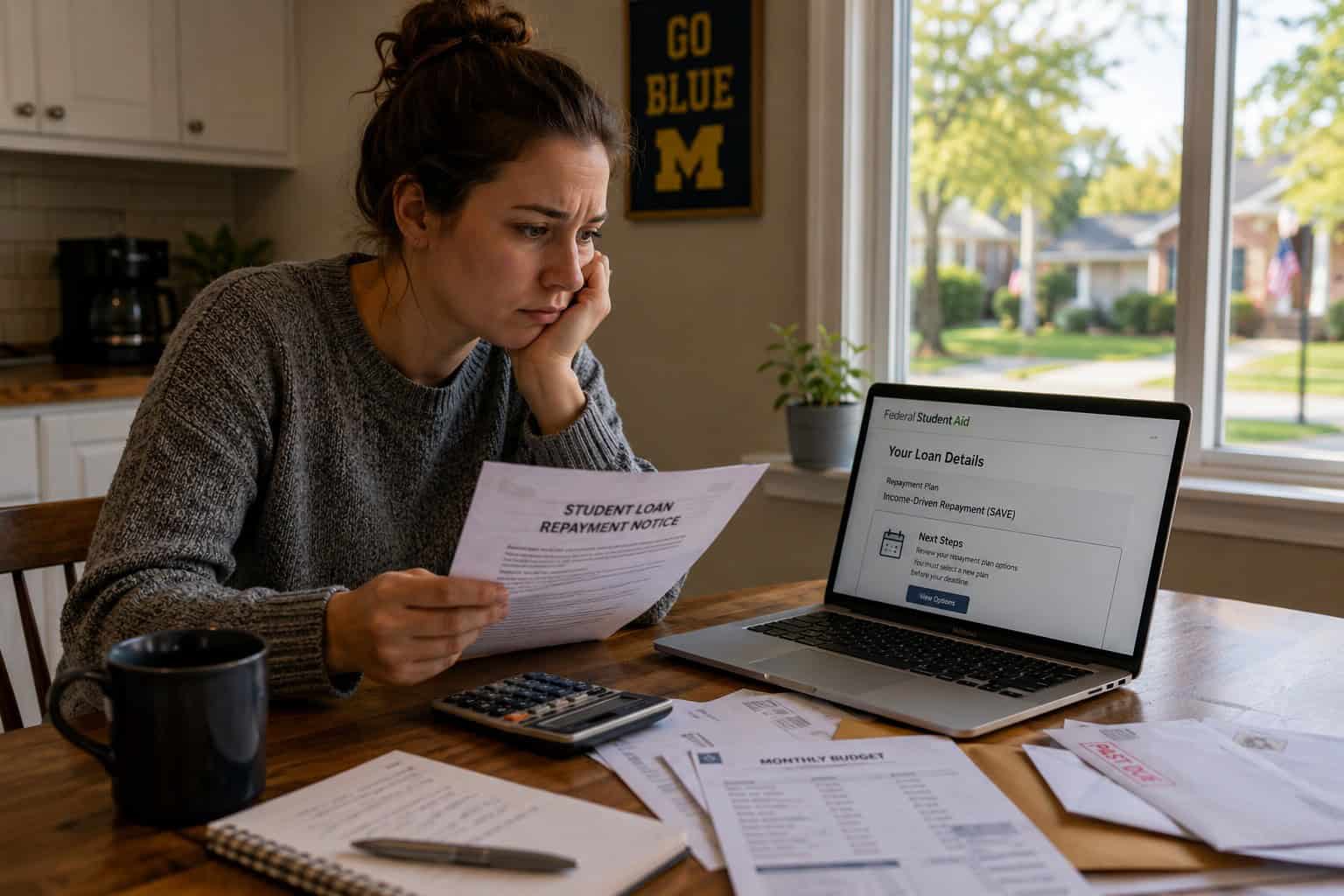

Federal Reserve data show the top 1 percent of Americans now own roughly 31 percent of the nation’s household wealth, while the bottom half own about 3 percent. Student loan balances have grown dramatically over the past two decades, while housing affordability has become one of the defining economic challenges facing younger Americans.

In Michigan, those national trends are reflected in household budgets every month.

Residential electric bills have climbed as utilities invest billions in new generation and grid modernization. Auto insurance premiums remain among the highest in the nation. Property taxes have increased in many communities as home values have risen. Grocery prices remain well above pre-pandemic levels, even as inflation has eased.

No single statistic proves the American Dream is slipping away.

Taken together, however, they raise an important question as America celebrates its 250th birthday:

Has the economic path that helped millions of Baby Boomers build wealth become more difficult for the generations following them?

The American Dream Has Always Evolved

When the Declaration of Independence was adopted in 1776, it promised liberty and the pursuit of happiness—not homeownership or retirement accounts.

Those ideas developed over generations as the nation expanded westward, industrialized and built what became one of the world’s largest middle classes.

By the end of World War II, a unique combination of rising wages, expanding suburbs, affordable higher education, federally backed mortgages and strong postwar economic growth enabled millions of Americans to purchase homes, accumulate savings and move into the middle class.

For many Baby Boomers, that became the practical definition of the American Dream.

Millennials entered adulthood under very different circumstances.

Many graduated into or shortly after the Great Recession. Home prices and rents increased faster than incomes in many metropolitan areas. College tuition and student debt reached record levels. Defined-benefit pensions largely disappeared from the private sector, while rapid advances in technology and, more recently, artificial intelligence began reshaping the labor market.

The result is not necessarily fewer opportunities—but different ones.

Today’s economy offers careers and businesses that previous generations could scarcely imagine. At the same time, the traditional milestones of financial security often arrive later than they once did.

By the Numbers

Homeownership

- Median age of a first-time homebuyer: 40 (record high).

- First-time buyers account for 21% of all home purchases (record low).

Wealth

- Top 1% of households own about 31% of U.S. household wealth.

- Bottom 50% own roughly 3%.

Education

- Student loan balances have increased substantially over the past two decades.

- College costs have risen significantly faster than inflation over much of that period.

Household Costs

- Housing affordability remains one of the nation’s biggest economic challenges.

- Household debt remains near record levels.

Michigan Snapshot

- Residential electric bills have increased over the past several years.

- Auto insurance premiums remain among the nation’s highest.

- Property taxes have risen in many communities.

- Grocery prices remain well above pre-pandemic levels.

Five Ways the Economic Landscape Changed

Economists point to multiple long-term factors rather than a single cause.

Housing construction has lagged population growth in many markets, contributing to higher prices. Higher mortgage rates have increased monthly payments for first-time buyers. Healthcare, childcare and higher education costs have grown faster than inflation over extended periods. Globalization and automation transformed manufacturing and many white-collar occupations. Artificial intelligence is expected to reshape the labor market further in the coming decade.

Tax policy, demographic changes, productivity growth and federal spending decisions have also influenced the nation’s economic trajectory. Economists continue to debate the relative importance of each factor.

What they largely agree on is that building wealth through homeownership has become more difficult for many younger Americans than it was for previous generations.

Looking Toward America’s Next 250 Years

Every generation has faced economic challenges unique to its time.

The question facing the United States today is not whether opportunity still exists. It clearly does.

The question is whether the traditional path to financial security—owning a home, building equity, saving for retirement and passing wealth to the next generation—is becoming harder to achieve.

As America begins its next 250 years, that may be one of the most important economic questions the nation must answer